Exit Strategies: IPOs versus SPACs

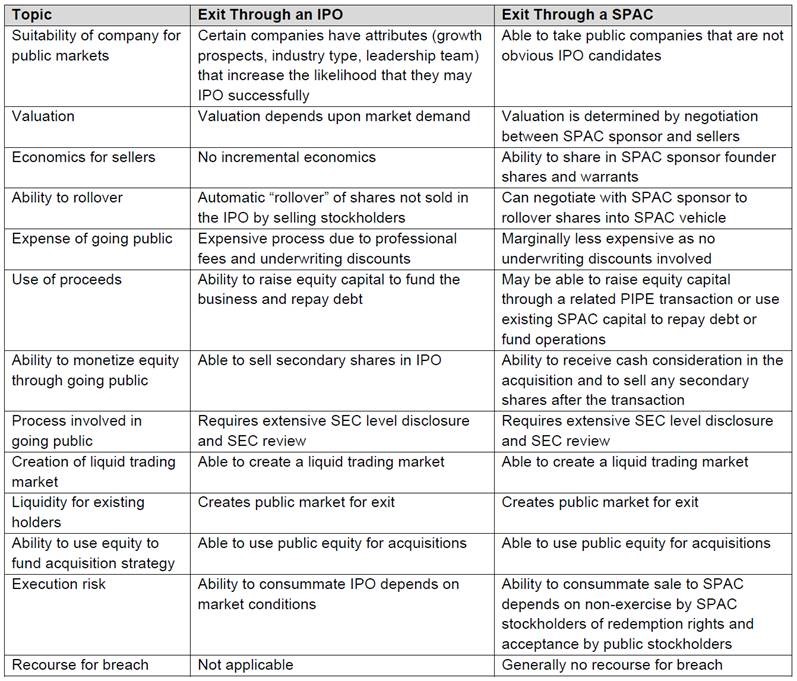

During the last several years SPACs have gone mainstream with brand name private equity sponsors raising SPACs and brand name private equity sponsors selling portfolio companies to SPACs. Private equity sponsors who are considering a public markets exit for their portfolio companies may want to consider the pros and cons of taking their portfolio company public through a traditional IPO or a SPAC. The chart below summarizes the principal similarities and differences between effecting a public market exit through an IPO or a SPAC.

As the chart above indicates, there can be significant advantages to structuring a public market exit for a portfolio company through a SPAC rather than a traditional IPO, including being able to customize the terms of the exit so that the selling sponsor can share in the founder shares and warrants received by the SPAC sponsor in connection with the formation of the SPAC and structuring the sale as an all cash deal or some combination of cash and stock. On the flip side, there is market risk in closing the SPAC transaction due to the redemption rights of the SPAC stockholders (although there is also market risk with an IPO obviously). The structure you choose will likely depend upon the nature of your portfolio company and your objectives.

Contributor(s)

More from the Private Equity Blog

Copyright © 2024 Weil, Gotshal & Manges LLP, All Rights Reserved. The contents of this website may contain attorney advertising under the laws of various states. Prior results do not guarantee a similar outcome. Weil, Gotshal & Manges LLP is headquartered in New York and has office locations in Boston, Brussels, Dallas, Frankfurt, Hong Kong, Houston, London, Miami, Munich, New York, Paris, Shanghai, Silicon Valley and Washington, D.C.